Why I started

I have two sons. They are fourteen and thirteen — the age I was when nobody taught me anything about money.

That sentence isn't a complaint about my parents. They did everything they knew how to do. They worked hard, they kept us fed, they sent me to a good college. Money was something you earned through work, saved a little of, and didn't talk about. That was the available wisdom in middle-class India in the eighties and nineties, and my parents passed it on the way every generation does — by example, and by silence.

I am, at forty-three, only just learning the things I wish I had been taught at fourteen. What compounding actually does to money over thirty years. The difference between a salary and an asset. Why the urge to buy a thing is almost never the same thing as needing the thing. These are not complicated ideas. But they have to be taught early to take, and we mostly don't teach them at all.

So when I started reading books on money a year and a half ago, and the ideas began to actually settle inside me, I made a decision. I was not going to let my own boys figure this out as late as I had. I was going to teach them what I had just learned — in small, ordinary, unforced ways, while they were still young enough that it could shape what felt natural to them.

This is what I've been doing.

The notebooks

The first thing I did was buy them two notebooks — one each — to track everything.

Then I started suggesting a handful of stocks and mutual funds I thought were worth getting into. They'd think it over, sometimes come back with their own ideas, and based on what they decided, I'd execute the purchases through my own account. (Their PAN card applications had hit a bureaucratic snag I eventually gave up trying to fix; the investments sit in my account on paper, but they are theirs in every other sense.) Each transaction — date, name, units, NAV, total units — they'd enter into their own notebooks, in their own handwriting.

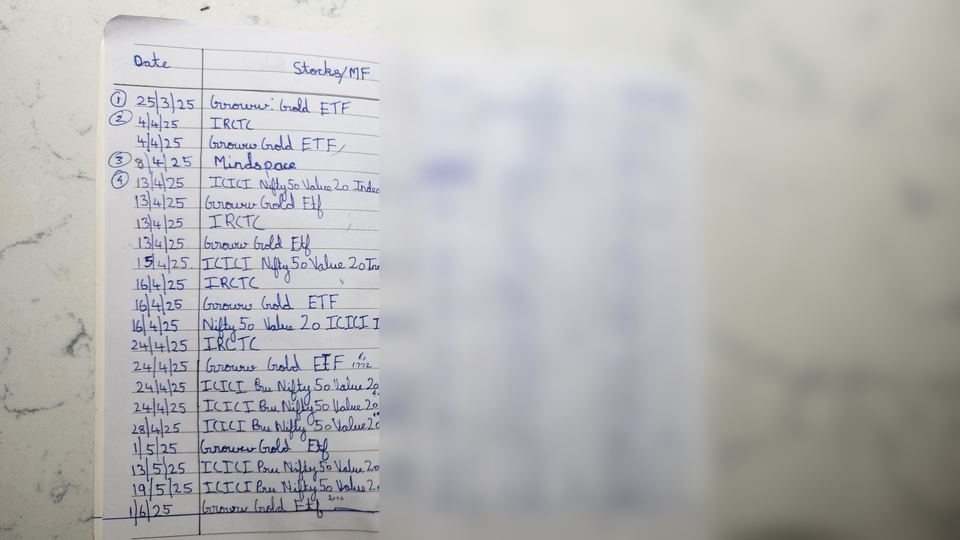

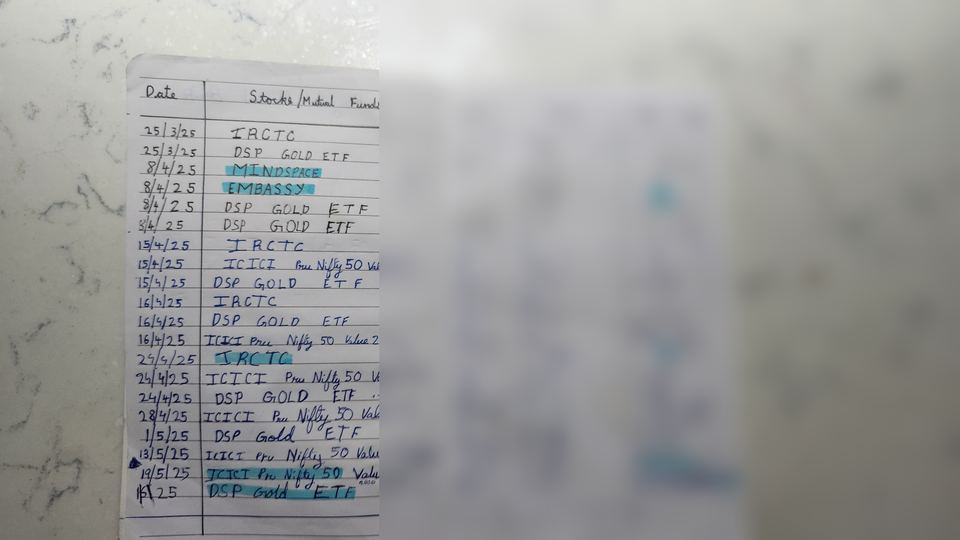

It is a small, slow, deliberate thing. But once a week they sit at the table, open their notebooks, and look at what their portfolios are doing. They are learning compounding from the inside — by watching it happen to their own money, in their own handwriting, not as a chapter in a school textbook.

Values blurred for privacy — but you can see the names of what they bought: IRCTC, Mindspace, Embassy REIT, Groww and DSP Gold ETFs, ICICI Pru Nifty 50 Value 20 Index Fund. A handful of real Indian instruments. Beginner positions, small amounts, real lessons.

The need-or-want question

The second thing I did was simpler, and probably more important.

Whenever they receive pocket money — from their uncles, grandparents, or us — and they want to spend it on something, a new game, a gadget, a pair of shoes — I ask them one question before they tap "buy":

Is this a need, or is this a want?

That single question, asked enough times, becomes a small muscle. They've started catching themselves now, mid-cart, asking it without me. And more often than not, they realise it's a want, and they end up moving that money into their investments instead. Watching the investments grow has quietly become more satisfying to them than the dopamine hit of buying.

The three-day rule

But here's the part that's worked better than anything else — the three-day rule. If, after the "need or want" question, they still feel they really want the thing, I tell them this: sit with it for three days. Don't buy it today. If at the end of the third day you still want it as badly as you did on day one — go ahead and buy it, with my full support. A desire that survives three days is a real one, and it deserves to be honoured.

Most things don't survive three days. The desire was an impulse, triggered by an ad, a friend's purchase, a moment of boredom. Three days later it's gone, and a part of them is quietly relieved they didn't act on it. But the things that do survive three days — those are real desires. Buying it then feels different. It feels like a chosen purchase, not a triggered one.

I think this is the single most useful thing I have taught them. The "need or want" question gives them awareness. The three-day rule gives them control. And those two together — at thirteen and fourteen — will compound over a lifetime in ways I genuinely can't predict yet.

If you are a youngster reading this and you don't have someone in your life teaching you this, here it is from me. Use it on yourself, starting today. Every purchase you are about to make — ask the question. If the answer is want, wait three days. That alone will save you more money over your twenties than almost any other single habit you can build.

What I hope they take from it

Some of this will fail. That's normal. They're teenagers — they will buy things they regret. They will forget the notebooks for weeks at a stretch. The need-or-want question will, occasionally, get an eye-roll. None of that worries me. What I am after is not perfection. What I am after is grooves — small repeated patterns that, by the time they leave my house at eighteen or twenty, will feel as natural to them as brushing their teeth.

I am writing this down now partly so it is here for them to read when they're older — when the questions start coming back to them with more weight. They may roll their eyes at fourteen. But somewhere in their twenties, when their first salary arrives and the world starts asking them what to do with it, I want this piece to be findable. Written by their father. Before he forgot what it felt like to be teaching them.

And if you have children of your own — or younger siblings, nieces, nephews, anyone in your life who looks to you for how to think about these things — the system is simple enough to copy. A notebook each. One question before every spend. Three days before you act on a want.

That is it.

— Rex

This article grew out of a section in my longer piece, Make Money While You're Young — an honest letter to anyone in their youth, or to a parent who wants to set their kids up well, on money, on time, and on why wanting to be rich is not the wrong thing to want. If you found this useful, you may want to read that one too.